Islamic banking has emerged as a fascinating alternative to conventional finance, blending religious principles with modern economic practices. This unique system, rooted in Sharia law, has grown from a niche concept to a global industry managing over $2 trillion in assets. But what makes Islamic banking tick, and how has it carved out its place in the modern financial landscape?

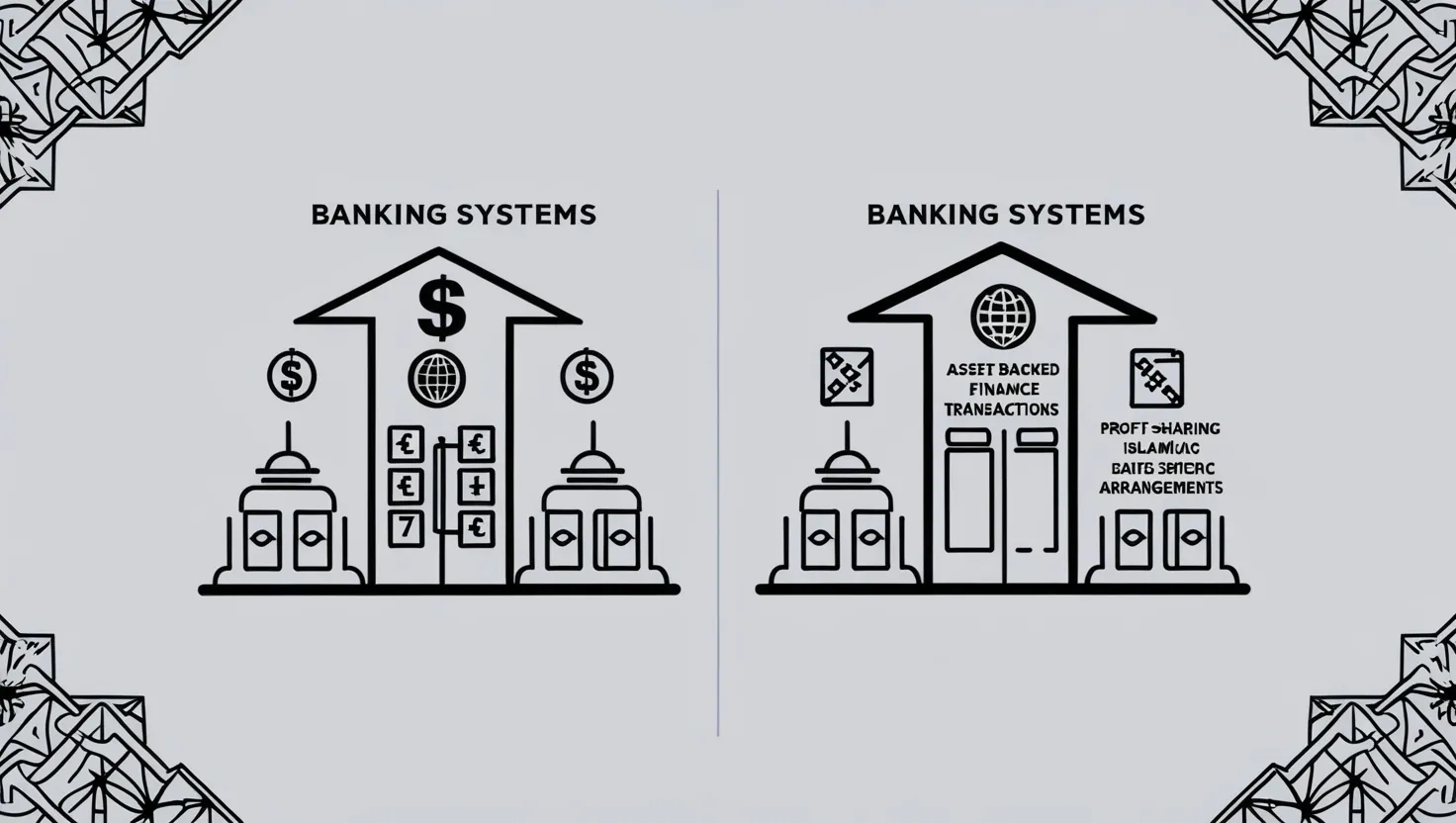

At its core, Islamic banking prohibits interest (riba), excessive uncertainty (gharar), and investments in industries deemed unethical or harmful. Instead, it emphasizes profit-sharing, risk-sharing, and asset-backed transactions. This approach aims to create a more equitable financial system aligned with Islamic ethical principles.

The modern Islamic banking movement took its first steps in the 1960s with the establishment of Mit Ghamr Savings Bank in Egypt and Malaysia’s Tabung Haji. These pioneering institutions demonstrated that banking could operate without interest while still generating returns for depositors and investors. The 1970s oil boom then provided a significant influx of capital, particularly in Gulf states, accelerating the industry’s development.

But how does Islamic banking actually work in practice? The system has developed a range of financial instruments to replicate the functions of conventional banking without violating Sharia principles. For example, mudarabah is a profit-sharing arrangement where one party provides capital and another provides expertise or labor. Musharakah functions as a joint venture, with all parties contributing capital and sharing profits and losses. Murabaha is a cost-plus financing structure often used for asset purchases.

“Money is not a commodity in Islam, but merely a medium of exchange.” - Umer Chapra

This quote encapsulates a fundamental difference between Islamic and conventional finance. Islamic banking views money as a means to facilitate trade and investment, not as a commodity to be bought and sold for profit.

The 2008 financial crisis unexpectedly thrust Islamic banking into the spotlight. While many conventional banks faltered due to excessive leverage and complex derivatives, Islamic institutions generally weathered the storm better. Their asset-backed approach and prohibition of speculative instruments provided a buffer against the worst effects of the crisis. This resilience caught the attention of regulators and investors worldwide, sparking increased interest in Islamic financial principles.

However, the Islamic banking sector faces ongoing challenges. How can it standardize practices across different regions and schools of Islamic thought? What tools can it develop for liquidity management given the restrictions on interest-based instruments? And perhaps most crucially, how can it balance strict adherence to religious principles with the need to offer competitive financial products?

Sukuk, often referred to as Islamic bonds, have emerged as a key innovation addressing some of these challenges. These instruments provide a Sharia-compliant way to raise capital and offer investors a fixed return without technically paying interest. The global sukuk market has grown rapidly, with issuances coming not just from Muslim-majority countries but also from the likes of the UK, Hong Kong, and Luxembourg.

Western financial institutions have increasingly recognized the potential of Islamic finance. Major banks now offer Islamic financial products, catering to Muslim populations in Western countries and to ethical investors attracted to the principles of risk-sharing and asset-backed financing. Financial centers like London, Singapore, and Hong Kong have introduced regulatory frameworks to accommodate Islamic finance, positioning themselves as hubs for this growing sector.

“The Islamic economic system is based on the paradigm of human well-being and good life, which stresses brotherhood and socio-economic justice.” - M. Umer Chapra

This perspective highlights the broader social and ethical goals underpinning Islamic finance. But can these lofty ideals truly be realized within a global capitalist system?

Understanding Islamic banking provides insights into alternative economic models that emphasize risk-sharing, ethical screening, and the connection between financial transactions and real economic activity. These principles have broader applications in sustainable and ethical finance, areas of growing importance in the wake of financial crises and increasing awareness of environmental and social issues.

The growth of Islamic finance also raises intriguing questions about the role of religion in modern economic systems. Can faith-based financial principles coexist with or even enhance secular economic models? How might the emphasis on ethical investing in Islamic finance influence broader trends in responsible investing?

As Islamic banking continues to evolve, it faces the challenge of maintaining its distinct identity while integrating with the global financial system. Will it remain a niche sector primarily serving Muslim populations, or could its principles gain wider adoption? Could elements of Islamic finance, such as its emphasis on risk-sharing and ethical screening, be incorporated into conventional banking to create a more stable and socially responsible financial system?

The story of Islamic banking is far from over. Its growth from a small-scale experiment to a global industry has already challenged assumptions about how finance can and should operate. As it continues to develop, Islamic banking may offer valuable lessons for the broader financial world, potentially influencing approaches to ethical investing, risk management, and financial stability.

What do you think? Could principles from Islamic banking improve the global financial system? Or are the differences between Islamic and conventional finance too fundamental to bridge?